Author: Spencer Siino

10-10-23

The market for Freight Broker License Bonds is barely keeping its head above water! Over the past six months, two of the top five surety carriers offering the BMC-84 bond, who together bonded approximately 20% of all freight brokers, have exited the market. The companies who continue to bond freight brokers have substantially increased premium rates and tightened underwriting, and it remains unclear whether these measures are enough to stem the bleeding.

Loss adjustment expenses (“LAE”) have long plagued sureties offering Freight Broker Bonds as highly informed truckers and factoring companies are quick to file claims as soon as payment is a day late, but in the past 12-18 months claims have skyrocketed due to a rapid increase in business failures and outright fraud.

At this rate, there won’t be any surety capacity left to support the logistics industry other than for the very best brokers, assuming underwriters can even determine good risks from bad in this unprecedented volatile market.

In this article, we dive into the causes of increased claims activity in the Freight Broker Bond market; analyze how the surety industry got into this predicament; share some of our company’s battle scars; and detail what we see as a solution to this fast-moving and complex problem.

What Is a Freight Broker Bond?

We hate to take a step back amidst all of the excitement, but for many participants in the surety industry, Freight Broker Bonds remain a bit of a mystery.

The Federal Motor Carrier Safety Administration (“FMCSA”) requires brokers moving freight loads across state lines to file a $75,000 Broker’s or Freight Forwarder’s Surety Bond. While modern society loves its acronyms and initialisms, “BFFSB” doesn’t exactly roll off the tongue, so we simply call this license bond requirement the Freight Broker Bond. The bond is required to protect interstate freight carriers, mostly trucking companies, from financial losses caused by licensed brokers for actions deemed negligent or fraudulent.

In lieu of a surety bond, which is classified by the FMCSA as “form BMC-84”, freight brokers, freight forwarders and property brokers can file a $75,000 cash deposit, known as the BMC-85 Trust Fund, with the FMCSA. The liability limit for the BMC-84 Bond and BMC-85 Trust Fund increased to $75,000 from $10,000 in 2013.

For any surety veterans or history buffs reading this article, the bond was formerly known as the “ICC Broker Bond” until the Interstate Commerce Commission, the first federal regulatory commission in U.S. history founded in 1887, was dissolved in 1996. For the record, most surety industry participants still called the requirement the ICC Broker Bond when our predecessor acquired BondExchange in 2012 and several surety brokers and underwriters continue to refer to the ICC Broker Bond today.

What’s Driving the Spike in Claims Activity on Freight Broker Bonds?

While there’s no shortage of sources of claims activity in the Freight Broker Bond market today, the primary drivers are supply-driven compression in broker margins and a substantial increase in criminal activity in the logistics sector.

Financier Henry Clews famously declared “the best cure for high prices is high prices”. While laissez-faire capitalism is not for everyone, this paradox has certainly played out, and then some, in the market for the services offered by freight brokers.

Freight brokers add value by solving logistical problems. The government’s response to COVID-19 created logistical nightmares and therefore increased demand for freight brokerage services. At the same time, consumers were stuck at home flush with stimulus checks with little choice but to order goods online, increasing demand for global shipments. This all led to a tight logistics market and strong gross margins and profits for freight brokers.

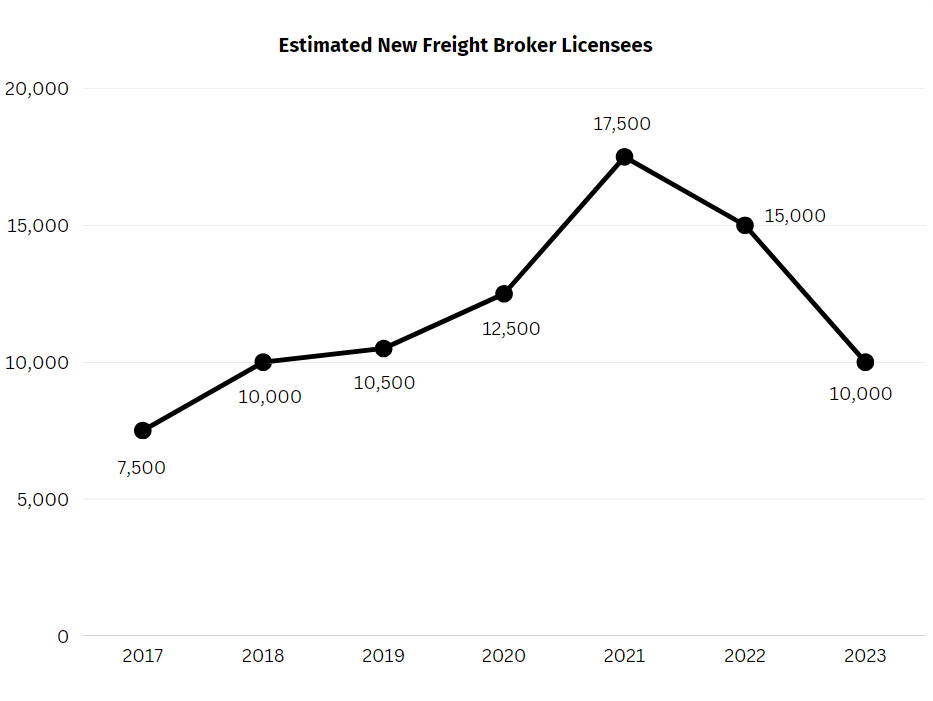

Unfortunately, many of those same consumers stuck at home and flush with stimulus checks were un(der)employed and watching YouTube. Considering an internet connection and a stimulus check can get you into the freight brokerage game, the result was an explosion of newly licensed freight brokers. There are now dozens of highly popular YouTube videos on “how to become a freight broker”, far more than necessary to support a total market of approximately 27,000 freight brokers, reflecting the likelihood that most new brokers are attracted to the promise of making income from their kitchens with little to no experience or upfront capital – not exactly a surety underwriter’s ideal bond applicant.

*Estimated total new licensees for the full year 2023 based on the first nine months of the year

*Estimated total new licensees for the full year 2023 based on the first nine months of the year

But bond them they did! As can be seen in the above chart, the number of newly licensed brokerages (all of them had to file a bond or place $75,000 into a trust account) increased by almost 70% from 2019 to the peak of the pandemic in 2021. Taken together the three pandemic years of 2020-2022 saw approximately 45,000 new brokerages enter the space, a 60% increase versus the three years before the pandemic and about 65% more than the entire market of active brokerages, implying an astronomical rate of business failure in the freight brokerage industry.

The result is a massive influx of inexperienced and undercapitalized freight brokers, each armed with $75,000 in surety credit, operating in a cyclical downturn in margins. In other words, we can expect business failures resulting in bond claims when the cash-strapped brokers first sell their receivables to factoring companies to raise cash and eventually cannot pay carriers for the low-margin loads they took on.

Criminals “Double” as Freight Brokers

An environment characterized by business failures, fewer loads per broker, and inexperienced new licensees promised the moon by YouTube influencers created the conditions for a rise in “double-brokering”, a gray area where brokers pose as carriers to bid on loads from other brokers. Double-brokering increases risk throughout the logistics value chain and can often lead to freight broker business failure, even when it’s not used as part of a scheme to defraud freight carriers, shippers, and surety companies.

An oversaturated market tempts brokers, particularly new businesses looking to build a customer base, to bid on loads from other brokers, further dividing already thin margins. Shippers and freight carriers, hungry for a deal in this inflationary environment, will sometimes forgo proper diligence especially when the bid includes early payment terms.

While double-brokering is about as criminal as jaywalking, like a gateway drug, the practice is just the start of criminal activity in the freight broker market.

The economic headwinds facing freight brokers are severe and, in a vacuum, would likely result in unacceptable loss ratios for surety companies. One might rightfully object that the surety industry has survived several economic and financial crises, many worse than this. However, surety bond carriers have never faced the systematic criminal fraud seen in the logistics arena in the past 18 months.

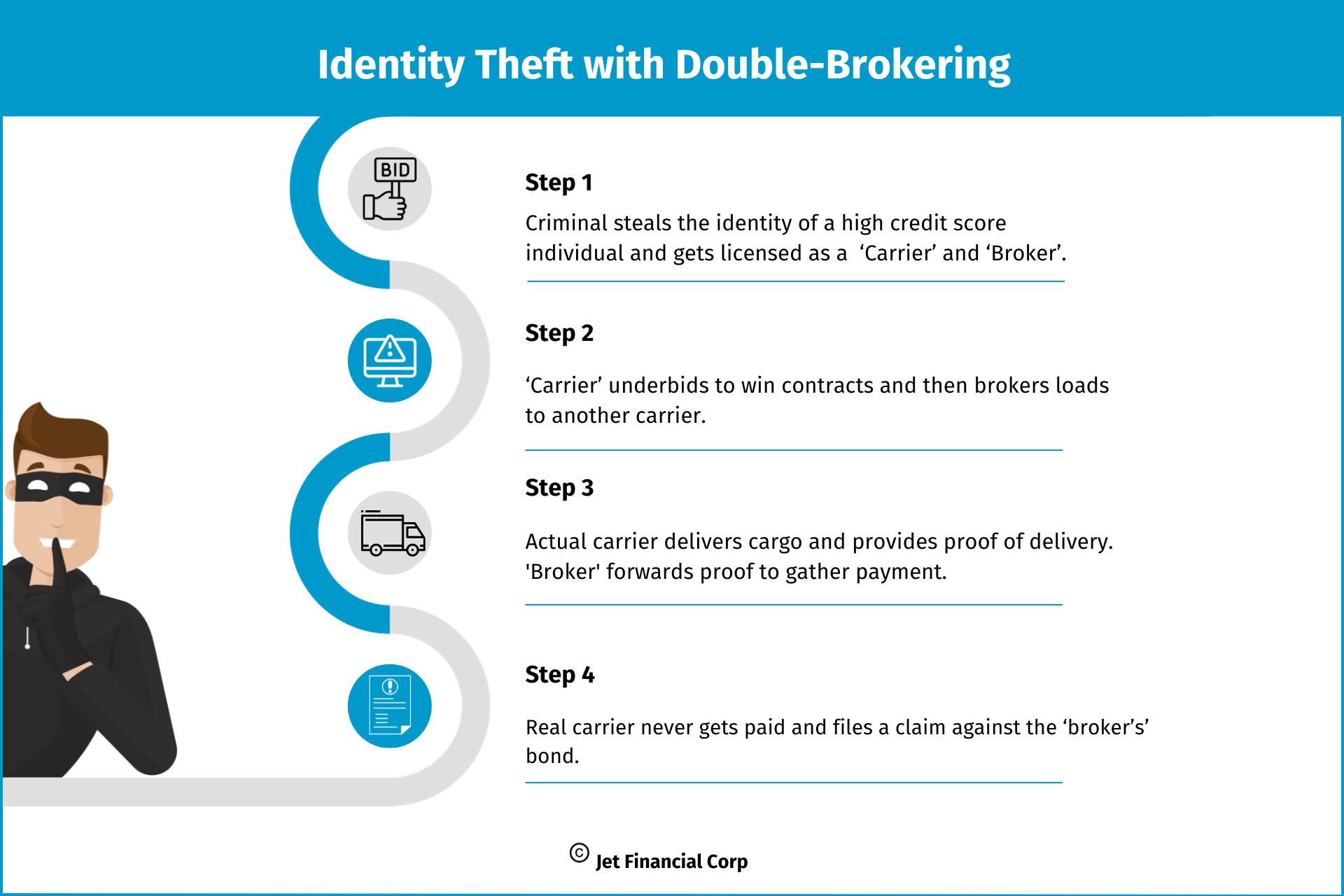

There are a number of scams that result in full limit ($75,000) claims on Freight Broker Bonds. For example, criminals are using stolen identities of individuals with excellent personal credit scores to apply for business licenses in the state where the identity was stolen and then freight broker and carrier licenses from the FMCSA. In most cases, surety bond underwriters are satisfied with Freight Broker Bond applicants with excellent personal credit who otherwise appear to be upstanding citizens, allowing fraudsters to purchase and file the $75,000 surety bond necessary to obtain a legitimate license number. Once the bond is filed, the fraudster has created a business entity, licensed by the federal government and the state in which the “owner” resides, legitimate in all respects except for the fact that the “owner” is entirely unaware that any of this has been established under his or her name.

Armed with the necessary licensing, the criminals will use their fraudulent motor carrier to bid on a load, usually with extremely attractive terms to the shipper or a legitimate broker, who think they are doing business with a legitimate carrier, to win the contract. The criminals will then use their fraudulent freight broker to book the load with a legitimate carrier (i.e., double-brokering), who delivers the goods to their destination, allowing the fraudulent broker to verify delivery with the shipper and demand payment from the shipper before paying the carrier. The truckers are supposed to get paid within 30 days of delivery and if not will file a claim on the surety bond on the 31st day following delivery. The criminals will double-broker as many loads as possible until the surety bond company cancels their bond, after which the fraudulent broker has 30 days to replace the bond before their license is revoked.

The upshot for the surety company is 50-100 bond claims for unpaid invoices totaling somewhere in the neighborhood of $100,000 on just one bad principal. In addition to paying out the full $75,000 limit, the surety company’s claims department must spend dozens of hours investigating each individual claim so that it can pay the valid claims on a pro-rata basis since the total claims exceed the bond limit. And no, the surety companies cannot deny this type of claim. Unlike an insurance policy, which can often be declared void if an insured lies on an application, the beneficiary of a surety bond is not the person who filled out the application and bought the bond. It’s the surety company’s job to vet the applicant.

After the Party Comes the Hangover

Between the fly-by-night dreamers and the out-and-out criminal rings, you’d think surety underwriters would have tired of the Freight Broker market. Instead, they gobbled up all of the premium from the afore-mentioned surge in new applicants and are now choking on claims and substantial claims handling expenses.

The problem has been a lack of effective underwriting. Surety carriers thought they could rely on personal credit scores and license checks as they often successfully do with other license and permit bond types. However, to navigate the rapidly changing logistics business freight brokers require working capital, experience, and integrity; if not, claims on their bond will rack up quickly. Add to these normal business risks the specter of identity fraud, and the traditional license bond underwriting model is just woefully inadequate to underwrite this bond type.

Exacerbating these problems is the fact that combined ratios in the Freight Broker Bond line are likely much worse than the pure loss ratios indicate due to the high LAE of the line. Most carriers commingle their claims handling with other transactional surety bond types and allocate their claims handling expense based on a percentage of premium or some other seemingly logical and easy-to-calculate metric. However, the volume of claims filed on Freight Broker Bonds taxes claims overhead at a much higher rate than the line’s relative amount of premium would imply. In fact, we believe the loss adjustment expenses on Freight Broker Bonds, if broken out from other bond types, often exceed the amount of actual claims payments on the bonds.

Aside from exiting the market altogether, it may be tempting for surety carriers to simply exclude freight brokers applying for a new license. For a variety of reasons, this strategy will not work either. Some freight brokers that have been in business for many years exhibit shifting payment history and use of factoring. Then there are the deliberate business failures that we refer to as “criminal retirement plans”. In fact, our surety company just experienced a full limit loss on a principal who had been in business for six years without a claim. Suddenly, the broker has 67 claims for individual unpaid loads totaling more than $280,000, 26 of which relate to a bond we issued very recently, and of course the principal has vanished. And it’s not as if we can simply pay these claims and move on. The 26 claims alone aggregated to $132,000, which means the truckers who did their job delivering loads are going to receive 56% of their claim amount as we are required to pay up to the $75,000 limit on a pro-rata basis. This is where it gets interesting (and expensive!) – we and the surety on the prior bond term must carefully investigate the validity of each of the 67 individual claims because if we don’t, legitimate claimants will get short-changed.

We believe that the surety industry should continue to provide credit to qualified freight brokers. The function of surety companies is to vet potential principals before entering the marketplace. If we all simply stop writing new brokers, then this crucial cog in the logistics industry will start to die. We believe surety providers exist not just to avoid risk, but to prudently shift bondable credit risk from industry participants that lack our specific skill set and capital base to surety companies that are equipped to manage and absorb the inevitable claims once we’ve thoroughly vetted the qualified from the unqualified.

Underwriters: Show Me Your War Face

We believe there are solutions available to write Freight Broker Bonds at acceptable loss ratios, even in the current low-margin environment and with landmines such as criminal fraud, not to mention the historically elevated cost of handling claims on these bonds. However, bond companies will have to exhibit far greater underwriting discipline, along with a dose of creativity, to properly vet principals and supply consistent surety capacity to freight brokers in this rapidly hardening market.

As discussed earlier in this article, credit-only underwriting inadequately gauges the risk of Freight Broker Bond principals. To write this bond at acceptable loss ratios, we believe surety carriers must employ full underwriting coupled with freight broker industry-specific criteria. “Full underwriting” of surety bonds typically involves reviewing business financial statements, but more is required to identify the unique risks facing freight brokers and properly price applicants.

Therefore, in addition to analysis of business financial statements, surety underwriters must integrate information from the Secretary of State, FMCSA, freight carrier and broker load boards, databases specific to freight broker vendor payment history and factoring companies, which play a vital role in the financial plumbing of the logistics industry.

For newly established freight brokers, business financial statements are generally unavailable. However, we know that freight brokers require working capital to operate sustainably. Therefore, surety underwriters should require bank and brokerage statements to incorporate some working capital metrics into underwriting newly licensed freight brokers, which given the high rate of business failure should also require a higher rate structure relative to their more established peers.

As for the recent problem of identity theft, we believe it is essential that surety underwriters verify the identity of their applicants via facial recognition software paired with a clear copy of government-issued identification, or have a trusted agent vouch for their identity. Unfortunately, a picture or scanned copy of a driver’s license alone will not suffice as many of the latest IRS scams involve capturing an individual’s government-issued identification so the criminals can pair the ID with the stolen credit on the dark web.

While necessary to curb the recent surge in loss ratios, the above measures only take us back to when this was a difficult bond type due to very high loss adjustment expense ratios. Therefore, to write this bond profitably on a fully loaded basis (i.e., including the true overhead cost of internal claims staff, not to mention agent commissions and underwriting staff), surety companies must invest in claims automation, customized for this bond type.

With Great Power…

We believe that the role of the surety industry in our economy is to properly vet businesses that require surety credit before they cause financial harm to the public and then to provide our financial guarantee in the event we get it wrong, which we will do from time to time. I know that my fellow surety executives take this responsibility very seriously. Failure on the part of a surety company to properly vet freight brokers causes unacceptable loss ratios, financial harm to honest trucking companies, and administrative headaches for agents and principals alike as appetites shift rapidly with inadequate underwriting. However, ours is a storied industry, filled with bright, honest and experienced people. With underwriting discipline and proper investments in updated processes and technology, we can honor our commitment to qualifying bond principals and do our part to clean up the troubled logistics industry.